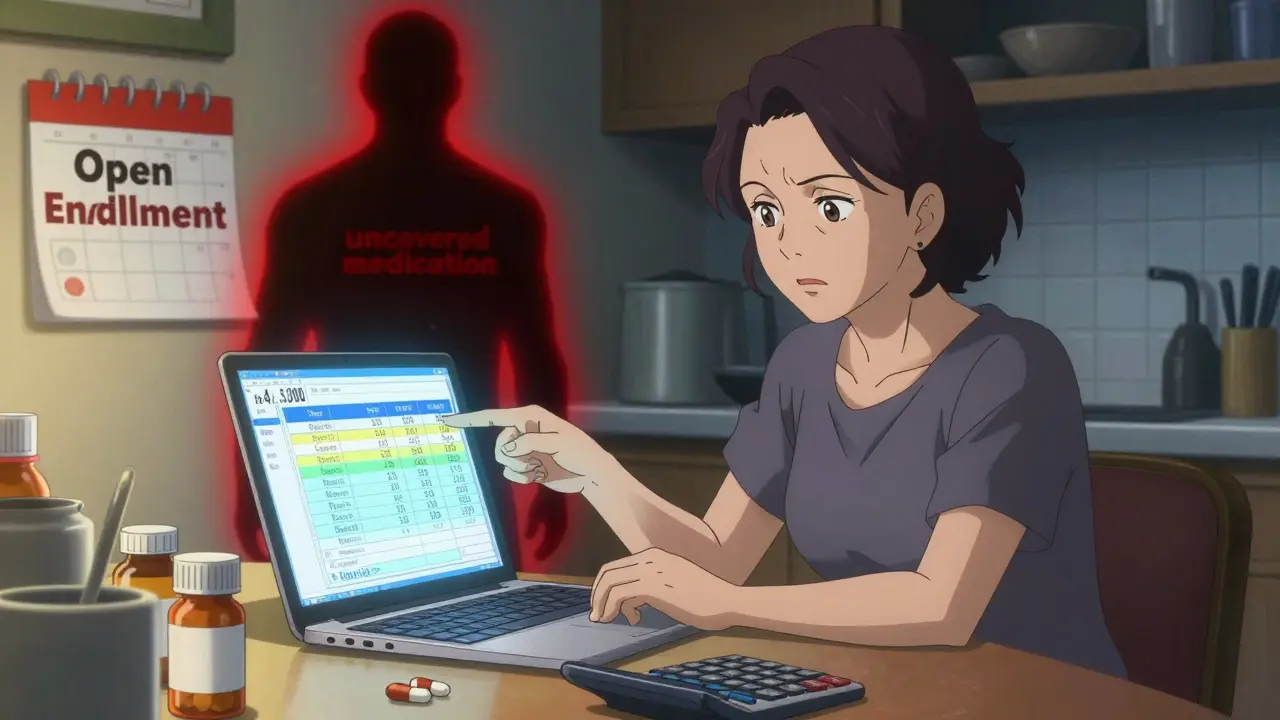

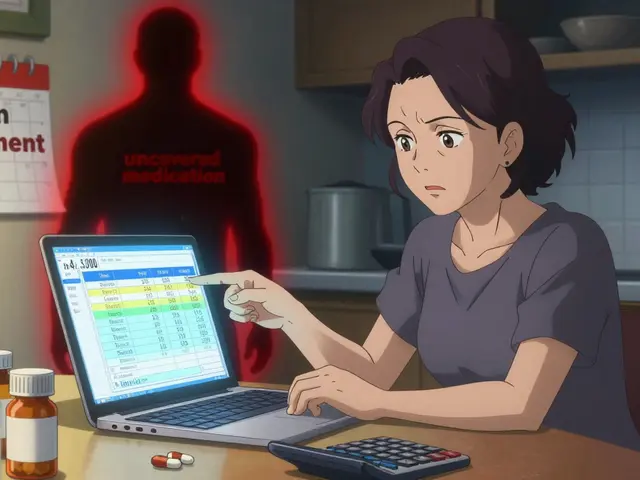

When you’re choosing a health plan, it’s easy to focus on monthly premiums and doctor networks. But if you take any regular medication-whether it’s for high blood pressure, diabetes, or even just an allergy pill-you could be leaving thousands of dollars on the table if you don’t ask the right questions about prescription insurance coverage. In 2023, over 66% of U.S. adults used at least one prescription drug. That means if you’re not checking your plan’s drug coverage, you’re gambling with your health and your wallet.

Is your specific medication on the formulary?

Every insurance plan has a list of covered drugs called a formulary. It’s not just a catalog-it’s a ranked system. Drugs are grouped into tiers, and each tier has a different cost to you. Tier 1 usually includes generics and costs around $10 per prescription. Tier 2 is preferred brand-name drugs, often $40. Tier 3 is non-preferred brands, which can jump to $100 or more. And Tier 4? That’s where specialty drugs live-medications for conditions like rheumatoid arthritis, cancer, or multiple sclerosis. These can cost over $1,000 per prescription, and you might pay 25-33% of the total price as coinsurance.Here’s the catch: just because a drug is FDA-approved doesn’t mean your plan covers it. A 2023 CMS survey found that 63% of people didn’t check if their specific medications were covered until after they enrolled. That’s how you end up showing up at the pharmacy with a $3,700 bill for a drug you thought was covered. Always enter your exact medications into your plan’s online tool. If you take insulin, statins, or thyroid meds, don’t assume-they’re not automatically covered.

What’s your out-of-pocket cost before coverage kicks in?

Many plans have a deductible for prescriptions. That means you pay 100% of the cost until you hit that number. Bronze Marketplace plans average a $6,000 deductible. Gold plans? Around $150. If you’re on multiple medications, a high deductible can wipe out any savings from a low monthly premium.Let’s say you take three monthly prescriptions totaling $300. With a $6,000 deductible, you’d pay $3,600 in the first year before your plan starts helping. With a $150 deductible? You’d pay $150, then $40 per refill. That’s a $3,450 difference. For someone on a fixed income, that’s life-changing.

Don’t just look at the deductible number. Ask: Does the deductible apply to prescriptions separately, or is it combined with medical costs? Some plans combine them, others don’t. If your medical visits are low but your meds are high, a plan with a separate drug deductible might save you money.

Are there step therapy or prior authorization rules?

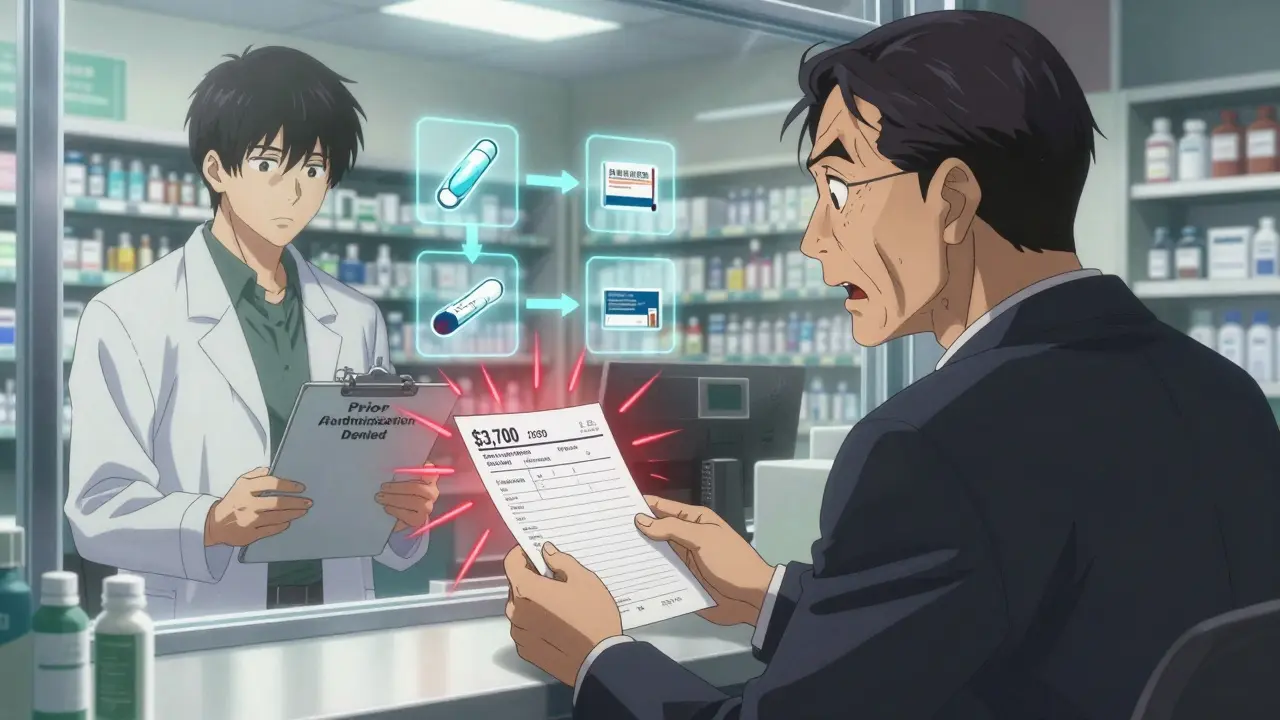

Step therapy means your plan forces you to try a cheaper drug first-even if your doctor says it won’t work for you. For example, if you need a biologic for psoriasis, your insurer might make you try three generic creams before approving the real treatment. That’s not just frustrating-it can delay care and make your condition worse.Prior authorization is even trickier. It’s when your doctor has to jump through hoops-submitting paperwork, proving medical necessity, waiting days or weeks-for your drug to be approved. In 2023, 28% of Medicare Part D prescriptions required prior authorization. One in five of those were denied the first time. If your medication needs prior auth, ask: How long does it usually take to get approved? What’s the appeal process if it’s denied?

Which pharmacies can you use?

Not all pharmacies are created equal. Most plans only cover prescriptions filled at in-network pharmacies. If you use an out-of-network pharmacy, you could pay 37% more. That’s not a small bump-it’s a full extra prescription cost.Some plans lock you into CVS, Walgreens, or Walmart. Others let you use mail-order services for a discount. If you’re on a long-term medication, mail-order can cut your costs in half. But if you travel often or live in a rural area, you need to know if there’s a network pharmacy nearby. Ask: Can I get my meds at my local pharmacy? What if I need an emergency refill while traveling?

What happens if you hit the coverage gap (donut hole)?

This only applies to Medicare Part D-but if you’re on Medicare, this is critical. The coverage gap used to be a scary trap: once you and your plan spent a certain amount on drugs, you had to pay nearly everything out of pocket until you hit a higher threshold. In 2024, you pay 25% of costs between $5,030 and $8,000 in total drug spending. That still adds up fast.But here’s the good news: starting in 2025, the donut hole disappears entirely. And insulin will cost no more than $35 per month. If you’re on insulin, this change alone could save you $400-$800 a year. Still, even with the new rules, you need to know how much you’re spending each month so you don’t get blindsided.

How do metal tiers affect your drug costs?

Marketplace plans are labeled Bronze, Silver, Gold, and Platinum. These aren’t just marketing terms-they reflect how much the plan pays for your care.- Bronze: Lowest premiums ($452/year), but highest out-of-pocket max ($9,450). Best if you rarely take meds.

- Gold: Higher premiums ($685/year), but much lower out-of-pocket max ($5,050). If you take 12+ prescriptions a year, this often saves you $1,842 compared to Bronze.

- Platinum: Highest premiums ($875/year), lowest out-of-pocket ($3,050). Ideal for people on expensive specialty drugs.

One user on Medicare forums saved $8,400 a year by switching from Silver to Gold because her insulin was covered at a $20 copay instead of $150. She paid $200 more in premiums-but saved $8,200 on meds. That’s not a trade-off. That’s smart planning.

What’s changing in 2025?

The Inflation Reduction Act isn’t just a headline-it’s changing your wallet. Starting in 2025:- Medicare Part D beneficiaries will have a $2,000 annual cap on out-of-pocket drug costs.

- Insulin will cost no more than $35 per prescription.

- Medicare will start negotiating prices for 10 high-cost drugs (20 more by 2029).

These changes mean that even if your current plan looks bad, next year might be better. But don’t wait. Use the Medicare Plan Finder tool now to see how your drugs will be covered under 2025 rules. If you’re on a specialty drug, your costs could drop by over $5,000.

When should you check this?

Don’t wait until you’re sick or your prescription runs out. There are two windows to review your coverage:- Marketplace Open Enrollment: November 1 to January 15. Use the HealthCare.gov tool to enter up to 15 medications and three pharmacies. It shows you exactly which plan saves you the most.

- Medicare Annual Election Period: October 15 to December 7. Use the Medicare Plan Finder. You must enter your drugs by NDC code-the 11-digit number on the bottle. Don’t guess. Type it in.

People who spend 20+ minutes checking their drug coverage save an average of $1,147 a year. That’s more than a month’s rent for many. It’s not complicated. Just open the tool. Type in your drugs. Compare. Change if needed.

What if your drug isn’t covered?

If your medication isn’t on the formulary, you have options:- Ask your doctor for a generic alternative.

- Request a formulary exception. Submit a letter from your doctor explaining why the drug is medically necessary.

- Appeal the denial. Most plans have a 60-day window to file an appeal.

- Switch plans during the next enrollment period.

One patient in Ohio was denied coverage for her MS drug. Her doctor wrote a 3-page letter. The appeal was approved. She saved $14,000 a year. It took two weeks. It was worth it.

Do all health plans cover prescription drugs?

Yes-under the Affordable Care Act, all Marketplace plans must include prescription drug coverage. Medicare Part D also covers prescriptions. However, employer-sponsored plans are not required to cover drugs, though 85% do. Always confirm your specific plan includes it.

Can I switch plans if my medication is dropped from the formulary?

You can only switch during Open Enrollment (November 1-January 15 for Marketplace, October 15-December 7 for Medicare). If your drug is removed mid-year, you can file a special exception request, but you’re not guaranteed coverage. Plan ahead by checking your formulary every year.

Why do some plans cover my drug but others don’t?

Each insurer negotiates separately with drug manufacturers. One plan might have a deal for a cheaper version of your medication, while another doesn’t. That’s why you can’t assume coverage based on a different plan. Always check your own plan’s formulary.

What if I can’t afford my copay?

Many drug manufacturers offer patient assistance programs. You can also check with nonprofit organizations like NeedyMeds or the Patient Access Network Foundation. Some pharmacies have discount cards. And starting in 2025, Medicare will cap insulin at $35 and out-of-pocket costs at $2,000-so if you’re on Medicare, wait until next year to re-enroll.

Is mail-order pharmacy better for prescriptions?

For maintenance drugs-like those taken daily-mail-order often costs less. You can get a 90-day supply for the price of two 30-day fills. Plus, you avoid pharmacy wait times. But make sure your plan allows it, and that the pharmacy is in-network. Some plans only offer mail-order if you commit to 90-day fills.

Eimear Gilroy February 27, 2026

Just spent 45 minutes entering my meds into HealthCare.gov. My insulin went from $180 to $35 under the new 2025 rules. I didn’t even know I was eligible. This post saved me a fortune. Thank you.

Ajay Krishna March 1, 2026

As someone who’s been on statins for 8 years, I can’t believe how many people don’t check formularies. I used to pay $90/month until I switched to a plan with tier 1 coverage. Now it’s $12. Simple math, folks. Don’t guess-check.

Sneha Mahapatra March 2, 2026

It’s wild how something so life-saving-like thyroid meds or insulin-can be treated like a luxury. I lost my job last year and almost skipped my dose because I didn’t know about patient assistance programs. I found NeedyMeds. They helped. No one talks about this enough.

Full Scale Webmaster March 3, 2026

Oh wow, this is such a masterpiece of misinformation. Let me break it down for you all. The Inflation Reduction Act? A scam. The $2,000 cap? It’s not a cap-it’s a bait-and-switch. They’re just shifting costs to manufacturers, who’ll raise prices elsewhere. And mail-order? Big Pharma’s way of locking you in. I’ve seen the spreadsheets. This whole thing is a shell game. You think you’re saving money? You’re just being groomed for the next phase of the healthcare consolidation playbook. Wake up.

Noah Cline March 5, 2026

Formulary tiers are a red herring. The real issue is PBMs. Pharmacy Benefit Managers. They’re the middlemen who negotiate rebates, then pass savings to insurers, not patients. Your $10 copay? That’s not because the drug is cheap. It’s because the PBM got a 70% rebate from the manufacturer. You’re still paying inflated list prices. The system is rigged. Ask your insurer for the net price-not the copay. They won’t tell you.

Lisa Fremder March 6, 2026

Why are we even talking about this? If you can’t afford your meds you shouldn’t be on them. Just get off the government teat and get a real job. My cousin works two jobs and pays full price. She’s fine. Stop whining.

Jimmy Quilty March 7, 2026

Wait-so you’re telling me the government’s going to negotiate drug prices? That’s a socialist takeover. Who’s to say they won’t pick the cheapest drug, even if it kills people? I know a guy whose MS drug was pulled because it cost too much. He’s in a wheelchair now. This is how you kill people. You think you’re helping? You’re just enabling dependency. The market should decide. Not bureaucrats.

Miranda Anderson March 8, 2026

I didn’t realize how much I was overpaying until I compared my current plan to a Silver plan with a separate drug deductible. I was paying $150/month for my antidepressant. Switched to a plan where it’s tier 1. Now it’s $10. I didn’t even have to change doctors. Took me 20 minutes on the tool. This should be mandatory info on every enrollment page.

Gigi Valdez March 10, 2026

It is important to note that while the article presents a comprehensive overview of prescription coverage considerations, one must also account for regional disparities in pharmacy access. Rural populations, particularly in the Midwest and Appalachia, often face significant logistical barriers to mail-order services and in-network pharmacies. Policy solutions should not assume universal broadband access or reliable postal infrastructure. Further research into mobile pharmacy initiatives may be warranted.

Byron Duvall March 12, 2026

Who even uses HealthCare.gov anymore? My cousin signed up last year and got billed $2,000 for a drug that was "covered." Turns out the plan changed the formulary mid-year. No one told her. Now she’s in debt. This whole system is a joke. They want you to think you’re in control. You’re not. You’re a number.

Brandie Bradshaw March 13, 2026

Let’s be clear: the real villain here isn’t the insurance company-it’s the pharmaceutical industry. They charge $1,200 for a drug that costs $12 to make. They lobby to block generic competition. They extend patents through tiny chemical tweaks. And now, with the $2,000 cap? They’ll just raise list prices so the 25% coinsurance still nets them a fortune. We need price transparency-not just coverage tweaks. Demand to see the actual cost of production. If they can’t justify it, break the patent.

Sophia Rafiq March 15, 2026

Mail-order is a game-changer if you’re on a long-term med. I get my blood pressure pills delivered every 90 days for $18. Same drug at CVS? $89. I used to hate the idea of mail-order-felt impersonal. Now I’m hooked. No lines. No waiting. Just a box on my porch. Pro tip: check if your plan offers free shipping. Most do.

Martin Halpin March 15, 2026

So you think this is about health? Nah. This is about control. They want you dependent on pills. They want you scared of skipping a dose. They want you checking formularies every year so you never question why your drug costs $500 when it was $10 in 2010. The real solution? Stop taking the meds. Go holistic. Go raw. Go alkaline. Your body doesn’t need all this junk. I’ve been off all prescriptions for 7 years. My cholesterol? Lower than ever. Your doctor’s not your friend. They’re paid by Big Pharma. Wake up.